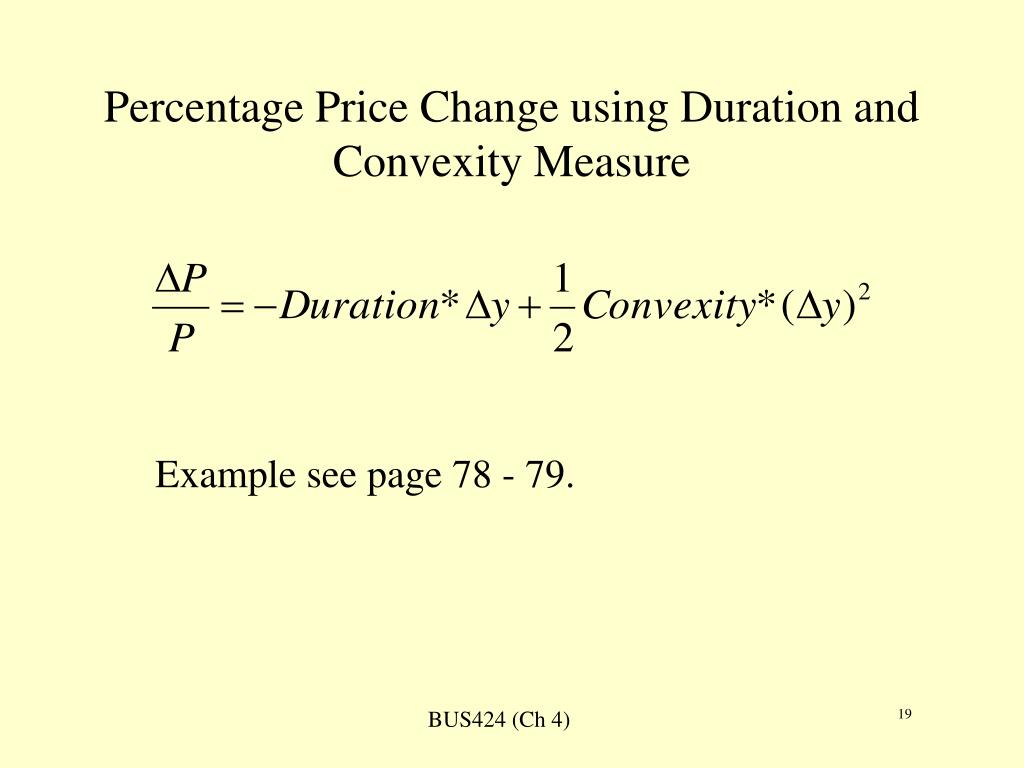

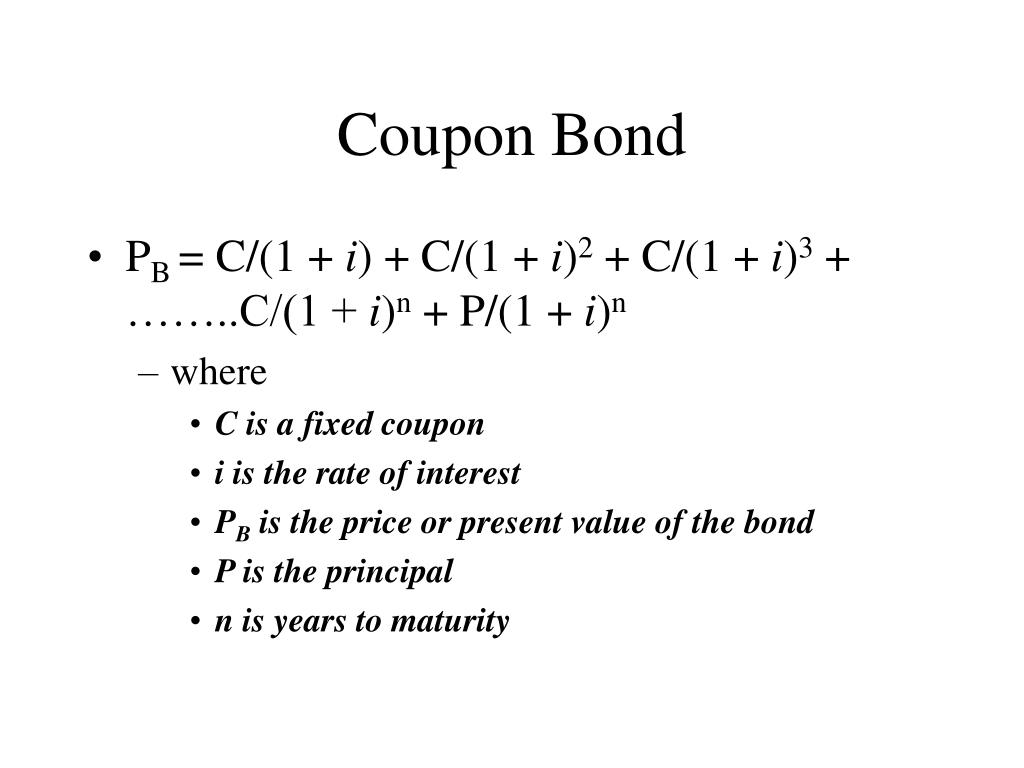

45 duration of a coupon bond

Dollar Duration - Overview, Bond Risks, and Formulas Dollar Duration. The change in the price of the bond for every 100 bps (basis points) of change in the interest rate. Updated August 31, 2021. ... It means that as interest rates fall, bond coupon rates increase. Short-term bonds are less sensitive to interest changes, while a 20-year long-term bond may be more sensitive to interest rate ... Duration of Bonds | Premium Bonds - PFhub Duration of the Two Basic Bond Types. Zero Coupon Bond: For a zero coupon bond, duration is the same as its maturity period. For a zero coupon bond, the fulcrum on the seesaw would be placed right under the bond's future value money bag at the maturity period (right most end of the plank), balancing its load right under. This is because the ...

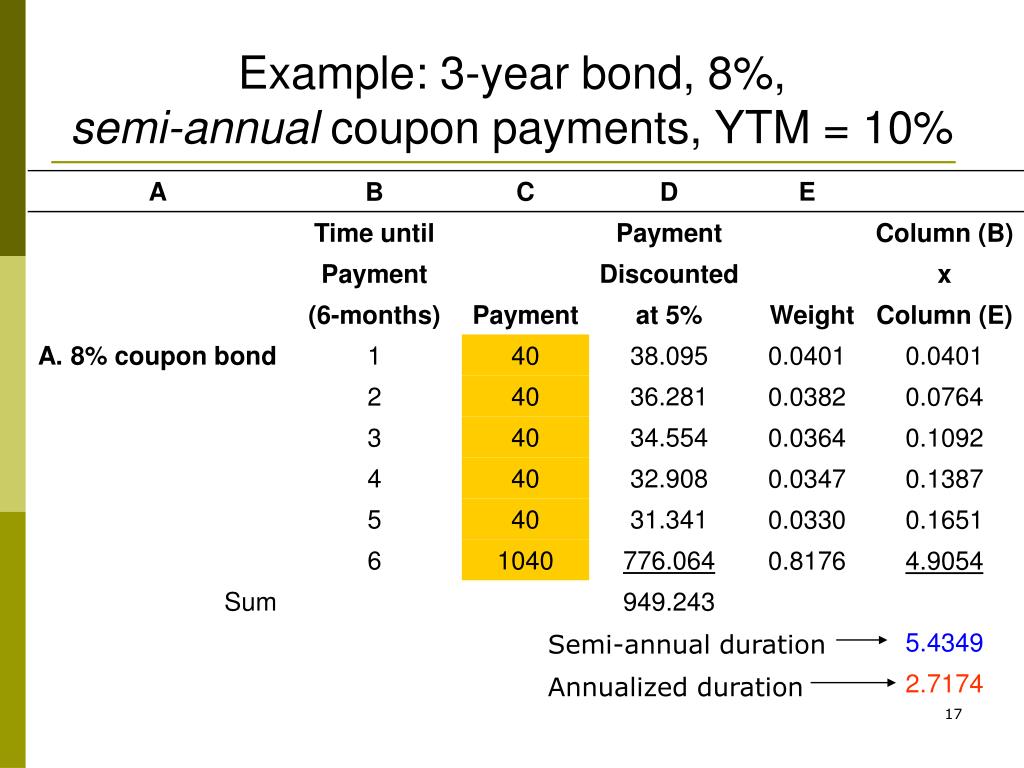

How to Calculate the Bond Duration (example included) Additionally, since the bond matures in 2 years, then for semiannual bond you'll have a total of 4 coupon payments (one payment every 6 months), such that: t1 = 0.5 years t2 = 1 years t3 = 1.5 years t4 = tn = 2 years

Duration of a coupon bond

What is the duration of a bond? and How to Calculate It? The model calculates the time the present value of cash flows from a bond takes to realize. The simplified formula for Macaulay duration is as below: Macaulay Duration = Sum of PV of cash flows [PV (CF 1) + PV (CF 2) … + PV (CF n )] / Market price of the bond See also Mortgage - Usages and How It Work Bond duration - Wikipedia The steps to compute duration are the following: 1. Estimate the bond value The coupons will be $50 in years 1, 2, 3 and 4. Then, on year 5, the bond will pay coupon and principal, for a total of $1050. Discounting to present value at 6.5%, the bond value is $937.66. How to Calculate Bond Duration - wikiHow Macaulay duration is the most common method for calculating bond duration. Essentially, it divides the present value of the payments provided by a bond (coupon payments and the par value) by the market price of the bond. The formula can be expressed as: In the formula, the variables represent the following:

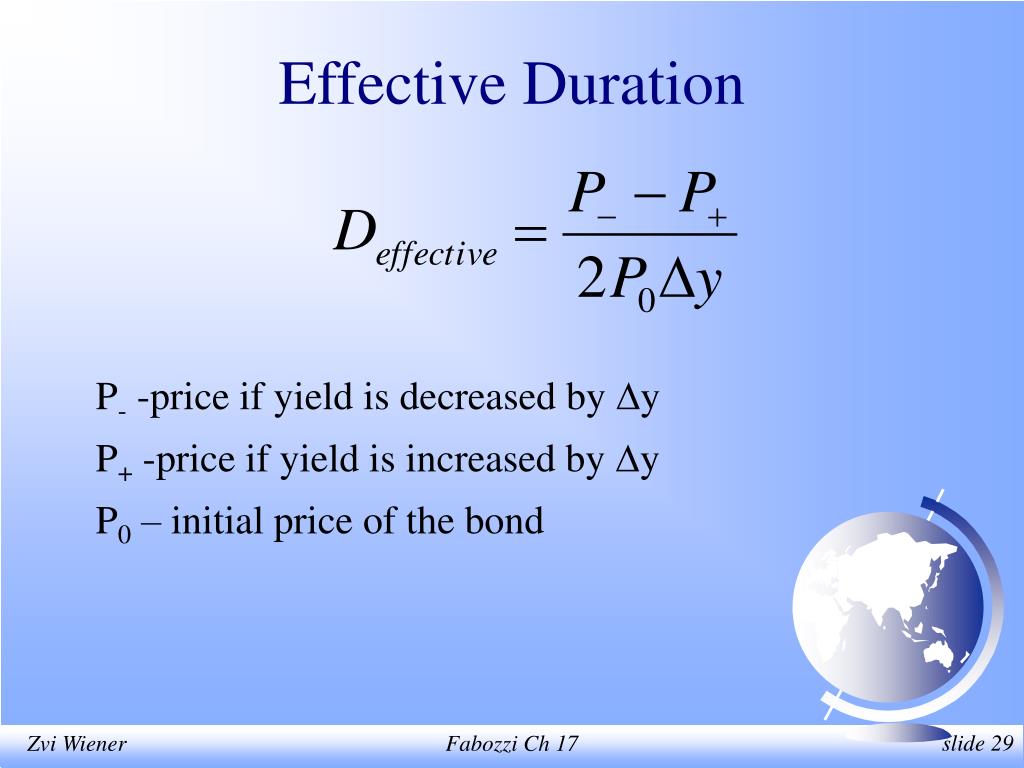

Duration of a coupon bond. Duration - Definition, Types (Macaulay, Modified, Effective) In other words, the measure takes into account possible fluctuations in the expected cash flows of a bond. The effective duration is calculated using the following formula: Where: V-Δy - The bond's value if yield falls by y% V+Δy - The bond's value if yield rises by y% V0 - The present value of all cash flows of the bond Δy - The yield change Coupon Bond - Investopedia Coupon Bond: A coupon bond, also referred to as a bearer bond, is a debt obligation with coupons attached that represent semi-annual interest payments. With coupon bonds, there are no records of ... Duration of a Bond | Portfolio Duration | Macaulay & Modified Duration Therefore, the Macaulay bond duration = 482.95/100 = 4.82 years. And Modified Duration= 4.82/ (1+6%) = 4.55%. The above calculations roughly convey that a bondholder needs to be invested for 4.82 years to recover the cost of the bond. Also, for every 1% movement in interest rates, the bond price will move by 4.55% in the opposite direction. Duration Definition - Investopedia The modified duration of a bond with semi-annual coupon payments can be found with the following formula: ModD=\frac {\text {Macaulay Duration}} {1+\left (\frac {YTM} {2}\right)} M odD = 1+( 2Y T...

Duration and Convexity to Measure Bond Risk - Investopedia However, for zero-coupon bonds, duration equals time to maturity, regardless of the yield to maturity. The duration of level perpetuity is (1 + y) / y. For example, at a 10% yield, the duration of... Modified Duration - Overview, Formula, How To Interpret Below is an example of calculating Macaulay duration on a bond. Example of Macaulay Duration. Tim holds a 5-year bond with a face value of $1,000 and an annual coupon rate of 5%. The current rate of interest is 7%, and Tim would like to determine the Macaulay duration of the bond. The calculation is given below: The Macaulay duration for the 5 ... What is the duration of a zero coupon bond? - Quora Originally Answered: How can I calculate the effective duration of a zero coupon bond? 1 - You have to know the current price 2 - You have to know its par value at maturity 3 - You have to know its yield to maturity 4 - If you know all the above, then you can use this familiar formula to calculate the term or duration: FV = PV * [1 + R]^N Duration Formula (Definition, Excel Examples) | Calculate Duration of Bond Calculation of the numerator of the Duration formula will be as follows - = 292,469.09 Therefore, the calculation of the duration of the bond will be as below, Duration Formula = 292,469.09 / 78,248.75 Duration = 3.74 years From the example, it can be seen that the duration of a bond increases with the decrease in coupon rate.

Bond Duration Calculator - Exploring Finance FV = Bond face value = 1000 C = Coupon rate = 6% or 0.06 Additionally, since the bond matures in 2 years, then for a semiannual bond, you'll have a total of 4 coupon payments (one payment every 6 months), such that: t1 = 0.5 years t2 = 1 years t3 = 1.5 years t4 = tn = 2 years What Is the Coupon Rate of a Bond? - The Balance A coupon rate is the annual amount of interest paid by the bond stated in dollars, divided by the par or face value. For example, a bond that pays $30 in annual interest with a par value of $1,000 would have a coupon rate of 3%. Regardless of the direction of interest rates and their impact on the price of the bond, the coupon rate and the ... Convexity of a Bond | Formula | Duration | Calculation For a Bond of Face Value USD1,000 with a semi-annual coupon of 8.0% and a yield of 10% and 6 years to maturity and a present price of 911.37, the duration is 4.82 years, the modified duration is 4.59, and the calculation for Convexity would be: Duration: Understanding the Relationship Between Bond Prices and ... Generally, bonds with long maturities and low coupons have the longest durations. These bonds are more sensitive to a change in market interest rates and thus are more volatile in a changing rate environment. Conversely, bonds with shorter maturity dates or higher coupons will have shorter durations.

PPT - Active Bond Portfolio Management Strategies PowerPoint ...

How to Calculate the Price of Coupon Bond? - WallStreetMojo Each bond has a par value of $1,000 with a coupon rate of 8%, and it is to mature in 5 years. The effective yield to maturity is 7%. Determine the price of each C bond issued by ABC Ltd. Below is given data for the calculation of the coupon bond of ABC Ltd. Therefore, the price of each bond can be calculated using the below formula as,

PPT - FINC4101 Investment Analysis PowerPoint Presentation, free ...

Coupon Bond - Guide, Examples, How Coupon Bonds Work Let's imagine that Apple Inc. issued a new four-year bond with a face value of $100 and an annual coupon rate of 5% of the bond's face value. In this case, Apple will pay $5 in annual interest to investors for every bond purchased. After four years, on the bond's maturity date, Apple will make its last coupon payment.

Modified Duration | Explanation, Example with Excel Template

Duration - NYU Stern For zero-coupon bonds, there is a simple formula relating the zero price to the zero rate. •We use this price-rate formula to get a formula for dollar duration.17 pages

Solved: Bond P Is A Premium Bond With A Coupon Rate Of 9.9... | Chegg.com

Bond Duration: What It Is and Why It Matters - Oblivious Investor A 5-year corporate bond with a higher yield will have an even shorter duration. For example, if sold for face value, a 5-year bond with a 5% coupon rate would have a duration of 4.49 years. Despite having the same maturity as the lower-yielding Treasury bond, it has a shorter duration. The reason for this is that a larger portion of the bond ...

Sober Look: 100-year bonds - for those who love convexity

Bond Duration Calculator - Macaulay and Modified Duration Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000 Coupon: 5% Current Trading Price: $960.27 Yield to Maturity: 6.5% Years to Maturity: 3 Coupon Payouts: One a Year

Bond Pricing on Coupon Days A bond pays a half yearly coupon at a rate ...

A 6% annual coupon, 30-year corporate bond was | Chegg.com Question: A 6% annual coupon, 30-year corporate bond was recently being priced to a yield of 7%. The Macaulay duration for the bond is 9.4 years. Given this information, the bond's modified duration would be a:9.55. b:9.24. c:8.79. d:7.78. If the market yield changes by 54 basis points, use Duration to estimate the change in the bond's price.

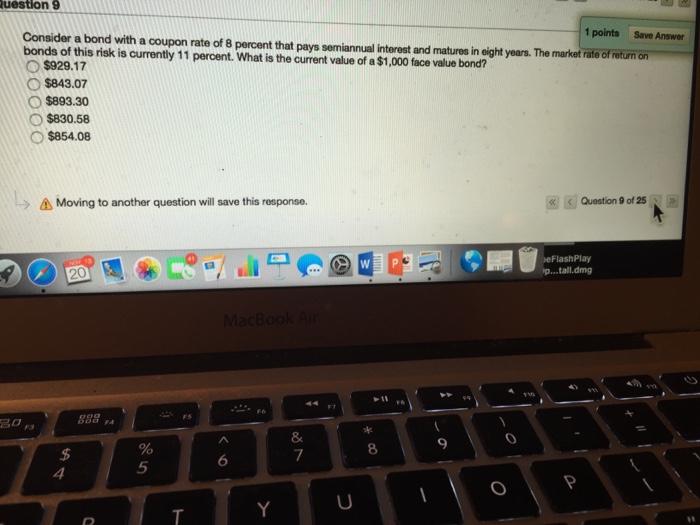

Solved: Consider A Bond With A Coupon Rate Of 8 Percent Th... | Chegg.com

Bond Duration | Formula | Excel | Example - XPLAIND.com Duration doesn't simply equal the term of the fixed income security except in case of a zero-coupon bond where it equals the term of the bond. In all other cases, where there are periodic payments in addition to the final balloon payment, duration is lower than the term of the fixed income instrument.

PPT - Duration and Convexity PowerPoint Presentation, free download ...

Macaulay Duration - Investopedia A coupon-paying bond will always have its duration less than its time to maturity. In the example above, the duration of 5.58 half-years is less than the time to maturity of six half-years. In...

PPT - Interest Rates and Returns: Some Definitions and Formulas ...

The Macaulay Duration of a Zero-Coupon Bond in Excel A bond's price, maturity, coupon, and yield to maturity all factor into the calculation of duration. All else equal, as maturity increases, duration increases. As a bond's coupon increases, its...

What is the duration of the coupon bond?

Duration | Definition & Examples | InvestingAnswers The lower the coupon, the longer the duration (and volatility). Zero-coupon bonds - which have only one cash flow - have durations equal to their maturities. 2. Maturity. The longer a bond's maturity, the greater its duration and volatility. Duration changes every time a bond makes a coupon payment, shortening as the bond nears maturity.

What is a coupon bond – COUPON

Understanding bond duration - Education | BlackRock It's lost some appeal (and value) in the marketplace. Duration is measured in years. Generally, the higher the duration of a bond or a bond fund (meaning the longer you need to wait for the payment of coupons and return of principal), the more its price will drop as interest rates rise. How duration affects the price of your bonds

What is the coupon rate of a bond – COUPON

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

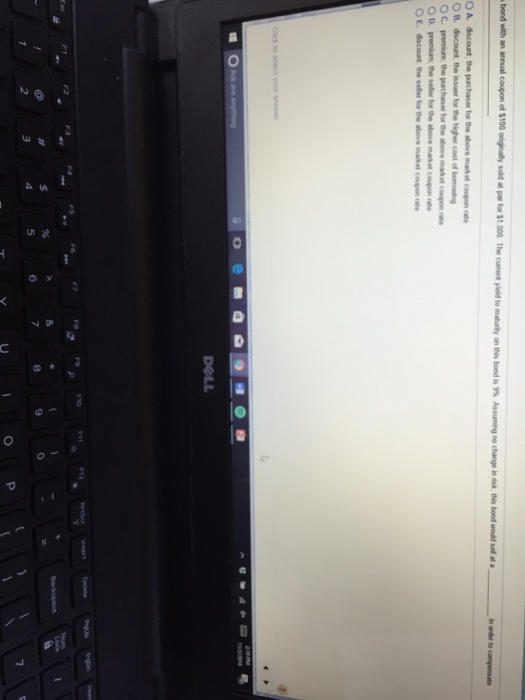

Solved: Bond With An Annual Coupon Of $100 Originally Sold... | Chegg.com

How to Calculate Bond Duration - wikiHow Macaulay duration is the most common method for calculating bond duration. Essentially, it divides the present value of the payments provided by a bond (coupon payments and the par value) by the market price of the bond. The formula can be expressed as: In the formula, the variables represent the following:

Modified Duration (Definition, Formula)| Step by Step Calcuation Examples

Bond duration - Wikipedia The steps to compute duration are the following: 1. Estimate the bond value The coupons will be $50 in years 1, 2, 3 and 4. Then, on year 5, the bond will pay coupon and principal, for a total of $1050. Discounting to present value at 6.5%, the bond value is $937.66.

Bond valuation

What is the duration of a bond? and How to Calculate It? The model calculates the time the present value of cash flows from a bond takes to realize. The simplified formula for Macaulay duration is as below: Macaulay Duration = Sum of PV of cash flows [PV (CF 1) + PV (CF 2) … + PV (CF n )] / Market price of the bond See also Mortgage - Usages and How It Work

Zero-Coupon Bond: Definition, Formula, Example etc. - Accountant Skills

Calculate the Price of a Coupon Bond - YouTube

Coupon Bond Paper Design ~ coupon

Post a Comment for "45 duration of a coupon bond"